The technology debate in insurance AI has largely settled. Document-heavy workflows, intake, and triage are good candidates for LLMs, but humans still own judgment.

The more interesting question is what will separate the insurance AI companies that will matter in ten years from the ones that won't. We've spent the past year pressure-testing our views with leaders across carriers, brokers, MGAs, and operators.

We believe it comes down to three things. The platforms that win will own actions and outcomes in a full feedback loop to drive better decisioning, earn trust via controlled auditability and verification, and rewire how insurance is sold.

Moats are built from feedback loops, not workflow automation alone

Intake, summarization, and routing tools are valuable, but they are also becoming table stakes. We think the more durable platforms will be the ones that connect workflow actions to downstream outcomes and use those connections to get smarter over time.

Did a submitted account ultimately become a policy? Did a claim escalate after an early intervention? Did an underwriting decision improve portfolio quality over time? Many workflow tools today cannot answer these questions. They measure activity, not impact.

The companies that build closed-loop systems, where actions and outcomes feed back into the system that improves future decisions, will likely have a fundamentally different product over time. A platform that has supported thousands of claims, captured the actions taken, observed the outcomes, and incorporated human review develops an evidence base that a new entrant could not easily replicate. That asymmetry compounds with each cycle.

We saw this logic early in our partnership with EvolutionIQ, which guides examiners toward better decisions in disability and injury claims – surfacing medical summaries, flagging escalation risk, and recommending next-best actions – and developed a durable informational edge in doing so. We saw a similar pattern in our partnership with Assured, which started with digital FNOL and expanded into a broader claims intelligence platform, leveraging a proprietary data layer to enable liability assessment and straight through processing of claims for some of the top 10 carriers.

As Don Vu, former CDAO at New York Life and Northwestern Mutual, put it: "AI becomes transformative in insurance when it does more than make existing workflows faster. The real opportunity is to reimagine how the business operates: where to focus underwriting attention, which claims need intervention, and where human judgment matters most in a workflow. Platforms that learn from outcomes and embed human oversight and governance from the start will be the ones insurers trust to take on more responsibility and drive step-function change over time."

Trust is frequently the gating constraint

In highly regulated industries like insurance, AI agents can automate a host of tasks. However, what determines whether these agents can be adopted at scale may ultimately come down to whether vendors can effectively navigate change management and trust.

Many of the most sophisticated operators we speak with are not asking "what can AI do." They are asking "what can we verify, audit, and defend."

AI that cannot surface the evidence behind a recommendation, flag uncertainty, document the decision path, and stay within defined guardrails is unlikely to earn expanded scope, regardless of accuracy. The companies likely to succeed will be those that design systems to earn trust progressively by creating auditability at every step, permissioned workflows where humans remain in the loop on high-stakes decisions, and a track record that gives operators the confidence to expand what the system handles over time.

We believe controlled autonomy is the architecture that scales in regulated industries.

Rethinking the distribution layer

Distribution, particularly the role of brokers and agents, is the backbone of the insurance industry. The U.S. P&C market runs through roughly 40,000 agencies and 15,000 brokers, the majority of them small and middle-market, sitting between roughly 4,000 carriers and the policyholders they serve. Independent agents and brokers placed 61.5% of all U.S. property and casualty premiums written in 2024, including 87.2% of commercial lines premium 1. The pattern extends to life insurance, which is often "sold, not bought." Independent distribution now represents six in ten dollars sold in U.S. individual life insurance, up from roughly half five years earlier 2. The life insurance industry also struggles with high agent turnover, with McKinsey estimating that 80% of life agents in the typical solo model quit within their first four years, creating a perpetual recruiting and onboarding burden 3. AI that expands the output of producers in the field could play a critical role in addressing one of the most persistent cost structures in the industry.

Taking it further, brokers and agents navigate a complex set of decisions, including the level of risk each carrier is willing to underwrite, what information they require, how best to position the account, and how to manage follow-up across fragmented systems. These steps are manual, inconsistent, and time-consuming. Many talented producers spend a disproportionate share of their time on logistics rather than relationships.

AI that helps producers package cleaner submissions, route risks to the right markets, and guide customers through complex purchase or renewal decisions tends to expand capacity and scales better decision-making, all while preserving brokers and agents' core strength of relationship-building.

We are also increasingly seeing a new class of vertically integrated startups going even further to own the distribution layer end to end, connecting carriers directly to customers, and streamlining the parts of the intermediary model where advice and relationship value are less central.

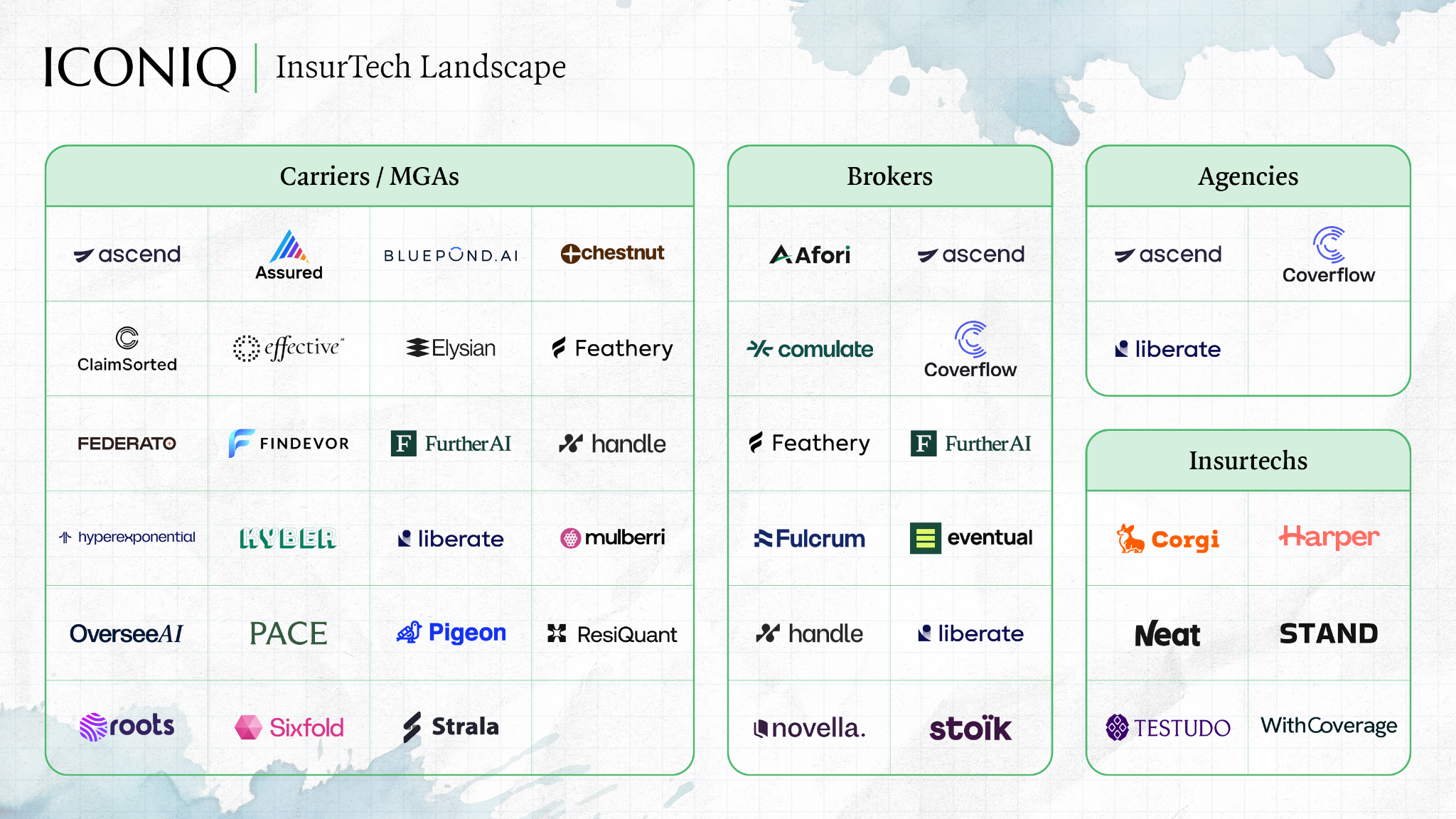

Across all three of these areas, we see a new wave of AI-native companies emerging. The map below captures the companies we think are doing the most interesting work today. It is not exhaustive, and the categories will evolve.

What we're looking for

We believe the best insurance AI companies will connect workflow to outcomes, earn autonomy through demonstrated trust, and treat distribution as a first-class problem. The most compelling implementations weave all three together.

A claims process that ingests a FNOL, cross-references policy details, flags escalation risk, surfaces a recommendation, and schedules follow-up – with a clear audit trail and fewer manual handoffs – is not just more efficient. It is building a proprietary data asset with every case it closes.

We believe the defining insurance AI companies of the next decade are being built now. If you are building in this space, please reach out to Sruthi Ramaswami (sramaswami@iconiqcapital.com), Carolyn Wu (cwu@iconiqcapital.com), and Brooke Chang (bchang@iconiqcapital.com).

Published:

May 27, 2026

.jpeg)

.jpeg)