AI Adoption Index

Many boards know their teams are using AI. Few can say where it's actually working. This is a framework for closing that gap.

The debate about whether AI drives real business outcomes is largely over. The question now is where it's driving them, how fast, and what changes inside the company as a result. That shift from "are we using AI?" to "where is it actually working?" is what prompted us to build the ICONIQ AI Adoption Index.

The AI Adoption Index

Over the past year, AI adoption has become a core indicator of company performance. The companies succeeding with AI tend to treat it as a core capability across product, engineering, go-to-market, and operations, with clear ownership and measurable progress.

But many board-level conversations about AI still sound the same: adoption is going well, tools are deployed, pilots are running; and when pressed on what's actually changed, the answers get vague.

That’s the gap the this index is built to help close. Rather than prescribing a single definition of success, the goal is to create visibility into how AI is actually being adopted across the business, putting a stake in the ground on measurement, and separating signal from noise. While AI impact can be difficult to quantify precisely, we believe not measuring it at all is a bigger risk. This framework forces explicit thinking about where AI is expected to drive outcomes and how progress will be assessed over time.

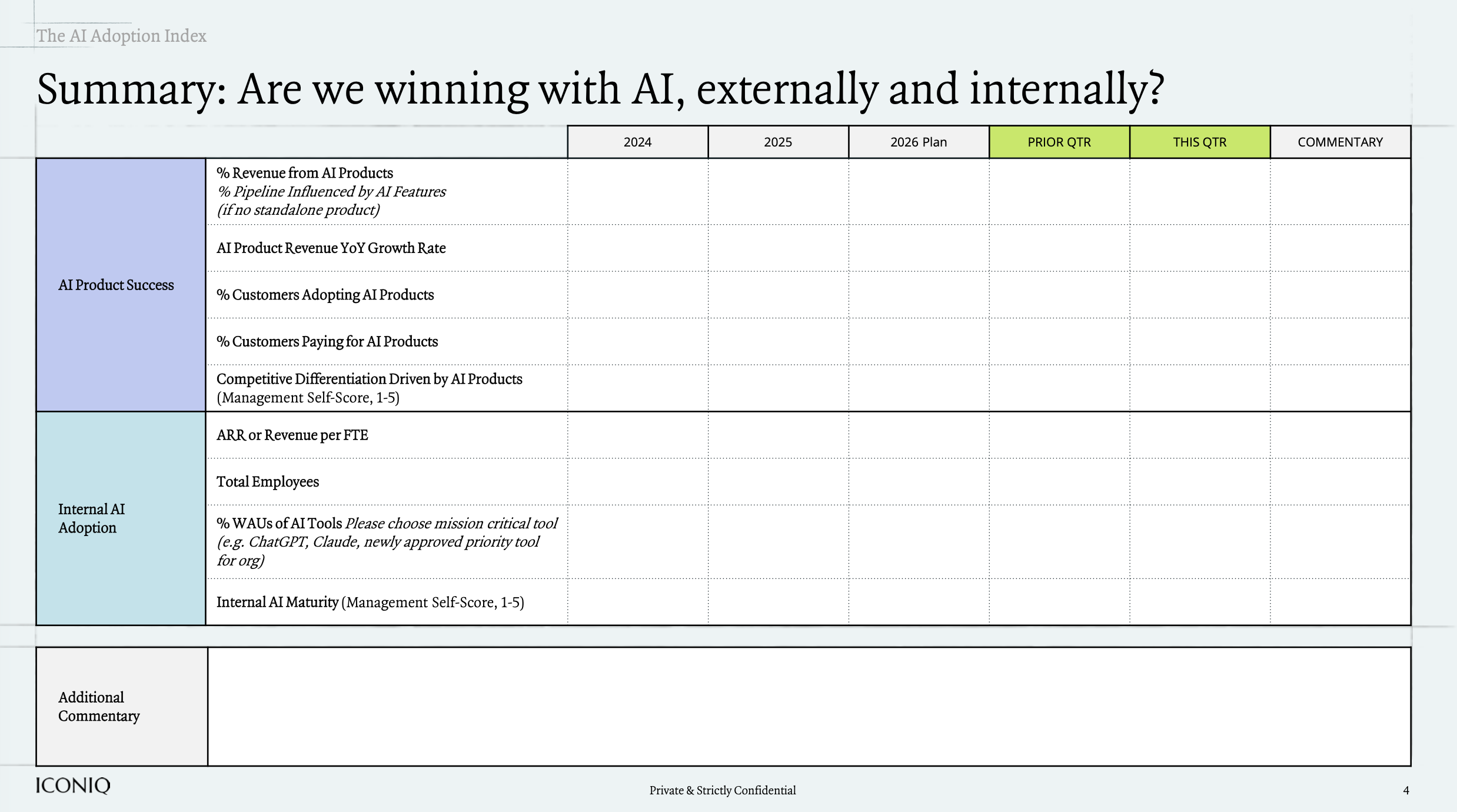

The template has two layers. A summary view keeps the board conversation focused (are we succeeding with AI, externally and internally?) without getting lost in the weeds. A set of functional pages for R&D, sales, marketing, customer success, and G&A goes deeper into the tactical inputs and leading indicators that functional leaders can actually influence, connecting day-to-day execution to the outcomes that matter at the board level.

The intent isn't to be comprehensive. What matters most will vary by business. Our recommendation is to update it quarterly, focus on trends rather than perfection, and pick a small set of metrics that best represent AI's intended impact on your company. Early quarters may be directional or estimated. Consistency and longitudinal improvement over time matters more than precision from day one.

What the data is telling us

At ICONIQ, we've been tracking AI adoption across our portfolio through CFO surveys, board decks, and direct company reporting.

Across the 38 portfolio companies we surveyed, 97-99% of employees have access to AI tools. Access is table stakes.

What separates leaders appears to be depth. In R&D, 86% of employees use AI daily and nearly half are power users (defined as 50%+ productivity gains). In GTM and G&A, daily usage sits around 70-74%, but power-user rates drop to 30%. The gap between access and meaningful productivity gain is where most companies are stuck.

R&D: the clearest ROI, and real structural implications

Engineering has moved the furthest and fastest among the functions surveyed. Developer velocity, review cycle time, and features shipped are up roughly 40% across the portfolio. QA and testing teams are seeing similar gains (around 40% time savings) with test coverage rising as a byproduct.

AI-generated code ranges from 25% to 88% of committed code at individual companies, with most clustering between 50-75%.

Tooling has also consolidated. Claude and Claude Code is the most widely deployed across coding, QA, code review, DevOps, and product design, used by 82% of surveyed companies for coding assistance. Cursor is a consistent second.

Productivity gains are also translating into structural changes. Several companies have reduced R&D headcount by 15-25% as a direct result of AI efficiency gains. Others have frozen net new hiring while maintaining or accelerating output.

The companies seeing the sharpest gains tend to have three things in common: a standardized toolset, a cultural expectation of daily use, and accountability for results. One CTO managed out engineers perceived as AI laggards. Another company pairs any engineer not hitting a 2x productivity gain with an internal mentor.

GTM: output up, headcount flat

Content generation shows the highest relative productivity gain of any GTM use case (about 55% on average) which helps explain why marketing teams have been early and enthusiastic adopters. Sales outbound and pipeline generation are up about 45% in productivity improvement. GTM enrichment and orchestration are in the same range. Sales coaching and forecasting trail at 20–25%. In sales, the impact shows up in pipeline activity. One company saw a 200% increase in deal meetings per AE per month. Others are reporting shorter sales cycles, higher ACV, and better win rates tied to AI-powered prospect research and outreach personalization.

In customer success, AI-driven ticket resolution is the clearest benchmark that we have identified. The average AI ticket resolution rate across companies tracking it is around 50%, and one company has reached 65% AI resolution with an 86% CSAT score. Several companies have grown their CS portfolio 60%+ without adding headcount, and at least one has deferred all new CSM hiring for 2+ years.

In marketing, the gains show up in throughput and cost. One company operates with half its prior marketing headcount and ships 20% faster. Another ran 43% more events with the same team.

G&A: the underrated opportunity

G&A functions tend to get less attention in AI conversations, but the data shows real productivity impact. Customer service leads at ~55% in average time and cost savings. Legal and contract review shows ~45% savings. HR and recruiting shows a 75% reduction in candidate screening time and a 50% reduction in time-to-fill. FP&A automation is earlier in maturity, with ~25% savings, but the operational shift from multi-week close cycles to same-day reporting is already happening at several companies.

The agentic AI angle is especially relevant in G&A. One company built an autonomous QBR deck pipeline that pulls customer metrics from multiple systems and outputs branded slides with no human steps. Several others have deployed AI-powered legal assistants handling routine contract review and legal inquiries. A healthcare company is using AI agents for clinical intake, claims review, and member navigation, with the expectation that AI will materially reduce frontline staffing requirements.

Several companies have formally adopted an "AI-first backfill strategy": when a role opens, the first question is whether AI can fill it. Others are increasing manager spans of control to 10+ direct reports, enabled by reduced administrative overhead.

What this all adds up to

The companies pulling ahead aren't necessarily the ones with the most AI tools or the highest seat counts. In our view, they are the ones that decided what success looks like, measured it, and held people accountable to it. The pattern across our portfolio appears consistent: access is nearly universal, but power-user depth separates leaders from the rest, and that gap is often a culture and accountability problem rather than a technology one.

The right question at your next board or team meeting isn't "are we using AI?". It's "where is it moving the business, and where has it stalled?"

Download our AI Adoption Index below.